How to safeguard your finances during a recession

Are you worried we might be going into recession – and how that will impact you financially? Find out how to safeguard your money.

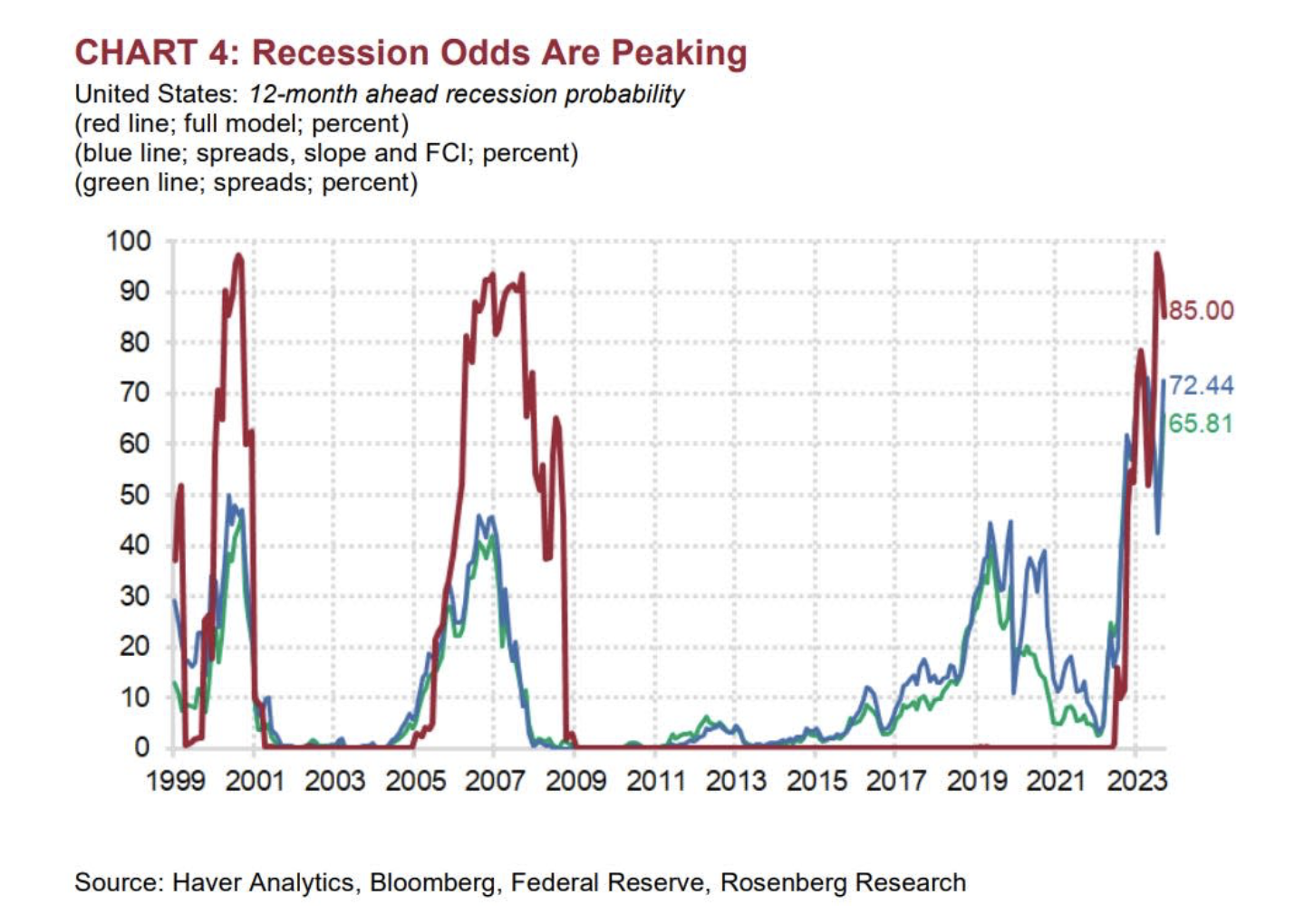

Nothing can be more financially crippling than experiencing a recession. Economist Davin Rosenberg reported that the United States has an 85% chance of recession this year. It’s the highest probable percentage since the Great Financial Crisis.

The question is: Are you financially ready for a possible recession? Don’t panic; Prepare instead. It’s time to improve your financial position as early as now!

Fret not – in this article we will share financial tips to help you prepare for a potential recession. Read on to learn how to safeguard your finances during this economic crisis.

Seven practical ways to protect your finances in a recession

The National Bureau of Economic Research (NBER) defines recession as “a significant decline in economic activity lasting for more than a few months.”

Traditionally, a recession is declared based on two consecutive quarters of decline as shown by indicators, such as gross domestic product (GDP) and unemployment rate.

But currently, NBER considers a recession a decline in activity across the economy for over a few months, as reflected in key factors like:

- GDP

- Real income

- Employment rate

- Industrial production

- Wholesale-retail sales

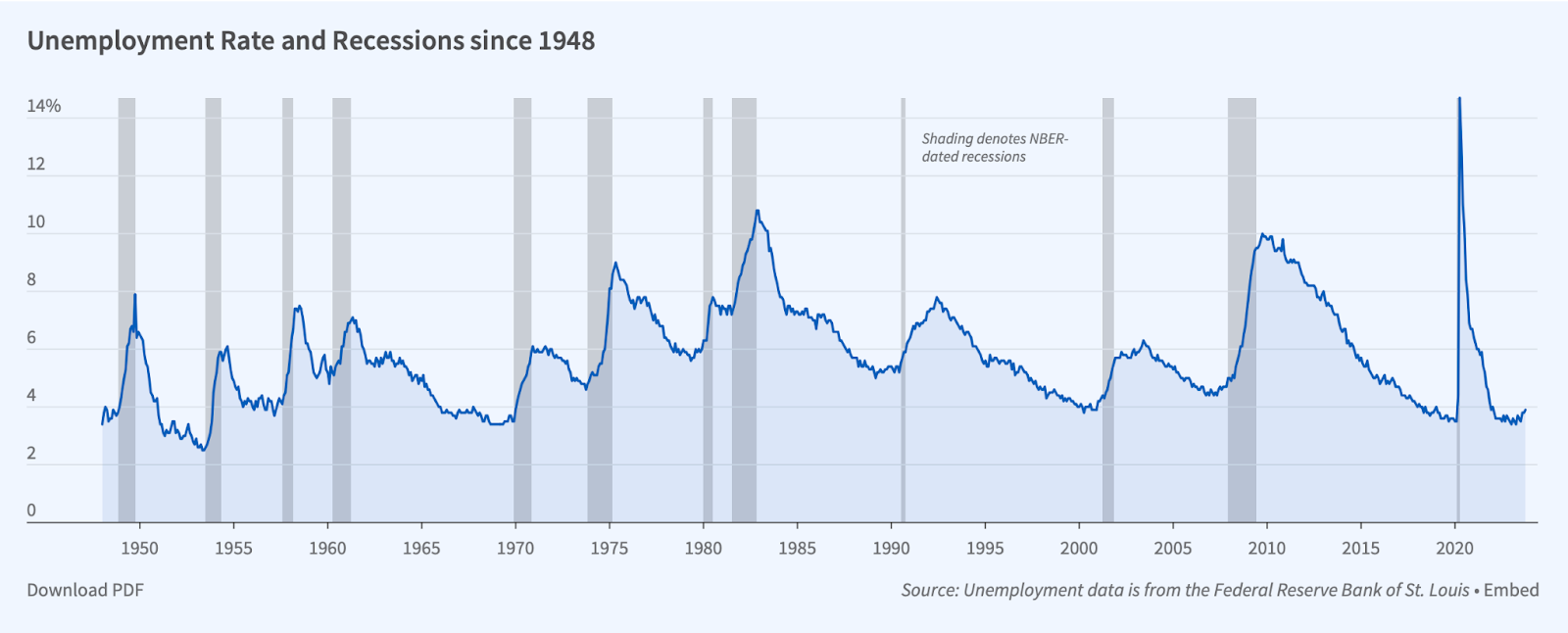

In recent years, the US has experienced some periods of recession. The country had the Great Recession from 2007 to 2009, one of the worst financial crises since the Great Depression. It also recorded the shortest one between February and April 2020.

Take a look at the country’s unemployment rate and recession period since 1948:

According to a recent CNBC’s All-America Workforce Survey, over 80% of workers are worried about a recession. It’s the biggest employee concern near-term at 83%, outweighing other worries, such as:

- Wages (74%)

- COVID-19 (62%)

- Pay cuts (46%)

- Layoffs (44%)

But how do you protect your finances from a potential recession? Don’t panic; better prepare. Here’s how.

1) Review and plan your finances

The possible recession is currently a forecast. The actual financial challenges have yet to come. This means you still have time to financially prepare for what lies ahead. Financial planning in times of economic uncertainty is key.

Jesse Galanis, Customer Relationship Manager at AllCrystal, suggests reviewing current finances and planning for a potential recession.

Galanis says, “With the recession predictions made by experts this year, you must be one step ahead. Start by assessing how much you’re receiving and spending regularly. Then, plan to maintain a consistent cash flow amid a financial crisis. Ultimately, it’s better to be prepared than sorry.”

2) Set a budget regularly

Budgeting is essential, with or without a recession. This involves checking how much you are earning regularly and planning how you’re going to spend it wisely. Start by improving your money mindset with this ultimate goal: Spend less than you earn.

Catherine Schwartz, Finance Editor at Crediful, recommends proper budgeting, especially during a recession.

Schwartz explains, “The rule of thumb is simple: Live within your means. Make it a habit to spend only what you have. Doing so makes you less likely to go into debt when a recession strikes. Remember, a debt begets more debts if you aren’t able to pay it off.”

3) Save money and build an emergency fund

Saving money is the first step to building a financial foundation, which later leads to financial growth and security. However, how can you survive a crisis, invest in financial resources, and grow your money if you don’t have enough savings?

Stephan Baldwin, Founder of Assisted Living, highlights the importance of an emergency fund to prepare for a possible recession.

Baldwin argues, “You must build savings equivalent to a six-month spending. During a recession, you can stay afloat for the next few months if you lose your job or your business suffers. That said, consider putting your money in a high-yield savings account and certificate of deposit.”

4) Cut your expenditures

As cited, proper budgeting ensures you spend less than you earn. If you think you’re spending more than you’re earning, consider ways to cut your expenses. For example, you can regulate water and energy consumption to reduce utility bills.

Jim Pendergast, Senior Vice President at altLINE Sobanco, suggests undergoing cost reduction, particularly during a recession.

Pendergast explains, “There are many ways to reduce your expenditures. Think of unused subscriptions and memberships to cut off. Consider alternatives to regular expenses, like preparing food for your lunch at work instead of eating out at a fancy restaurant. It’s just a matter of managing your expenditures wisely.”

5) Manage credit and pay off debts

There are many business credit and loan resources available to women entrepreneurs. But before taking the plunge, assess whether they are worth it and if they can help maintain your cash flow. If you already have a handful of credits to use and debts to pay, think of how you can manage them during a recession.

Many financial experts recommend debt consolidation to prepare for a recession.

To do this, get a low-interest loan that will provide you with a lump sum of money. Then, use this to pay all your other debts so that you can manage your finances better. Meanwhile, consider ditching credit cards with higher interest rates. Use those only for necessary expenses that won’t break your bank.

6) Think of long-term investments

Your money doesn’t have to sit in the bank used only for emergency situations and lifestyle plans. What better way to boost your finances than to grow your money through investments? However, think of how you can manage them long-term and should there be a recession. Allocate diversified assets to your portfolio!

Morgan Taylor, Co-Founder of Jolly SEO, underscores the importance of investment diversification.

Taylor explains, “If you own a house and have savings, you’re on the right track. You already have some money in real estate and some in your bank. However, invest in assets that increase in value, such as stocks and bonds. Also, employ the dollar-cost averaging strategy to reduce the volatility impact on your investments.”

7) Stabilize your income source

Your financial stability depends on your income source, whether employed or running a business. It’s a good idea to have an extra source of income to prepare for a possible recession. Consider side hustles, such as freelance work, affiliate marketing, and selling on e-commerce platforms, even if you’re 50 years old and above.

Brooke Webber, Head of Marketing at Ninja Patches, recommends diversifying income streams.

Webber argues, “A recession can potentially cripple your finances. Think of getting laid off from work or having low sales revenue during a financial crisis. But if you have another source of income, you won’t get massively impacted and will continue to survive.”

Prepare for a recession and protect your finances

A decline in economic activity impacting employment rate and household income is often inevitable. However, there are ways to prepare for a recession and protect your finances.

That said, consider the financial tips shared by some business experts above. To wrap up:

- Assess your finance

- Create a budget

- Save money

- Reduce expenses

- Pay debts

- Manage investments

- Establish an income stream

With all these in mind, you will financially survive and thrive even during a recession. In short: Don’t panic; prepare!